Press Release

Griffon Corporation Announces Fourth Quarter and Fiscal 2009 Operating Results

Reports 4Q 2009 Continuing Operations EPS of $0.21 vs. Year-ago Loss of $0.20

Full Year 2009 Continuing Operations EPS Increase to $0.37 vs. $0.00 in 2008

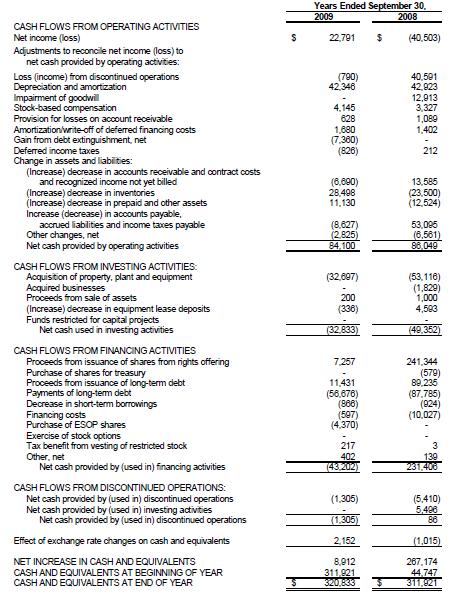

Griffon Generates Full Year 2009 Operating Cash Flow of $84 million

Book Value Increases to $11.53 per Share

NEW YORK, NEW YORK, November 19, 2009 – Griffon Corporation (NYSE: GFF) today reported operating results for the fourth quarter and fiscal year ended September 30, 2009.

Fourth Quarter 2009

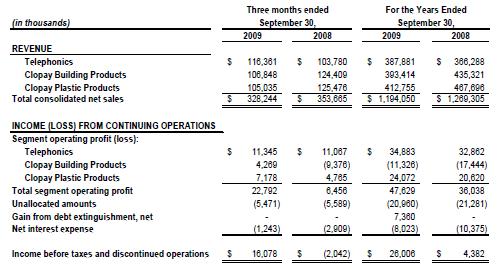

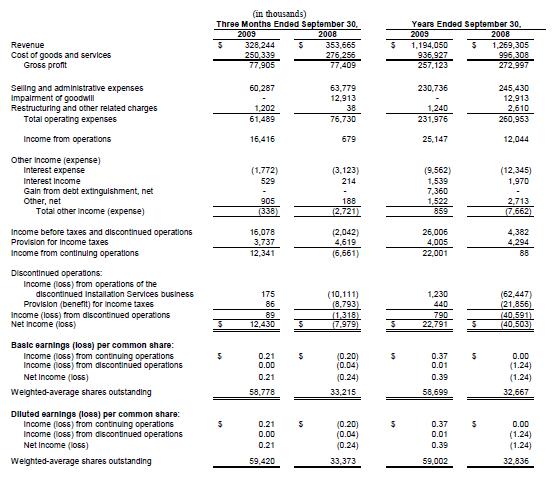

Revenue for the 2009 quarter was $328.2 million, compared to $353.7 million in 2008. Income from continuing operations for the current quarter was $12.3 million, or $0.21 per diluted share, compared to a loss of $6.7 million, or $0.20 per diluted share, last year. In the 2008 quarter, the Company recorded a $12.9 million goodwill impairment charge related to the Building Products segment; excluding this charge, fourth quarter 2008 income from continuing operations would have been $6.3 million, or $0.19 per diluted share. In 2008, there was a loss from discontinued operations of $1.3 million or $0.04 per diluted share; in 2009, results of discontinued operations were immaterial. Net income for the 2009 quarter was $12.4 million, or $0.21 per diluted share, compared to a loss of $8.0 million, or $0.24 per diluted share, in 2008. Diluted shares used for per share calculations were 59.4 million in 2009, compared to 33.4 million in 2008, an increase of 78% resulting primarily from the 2008 rights offering.

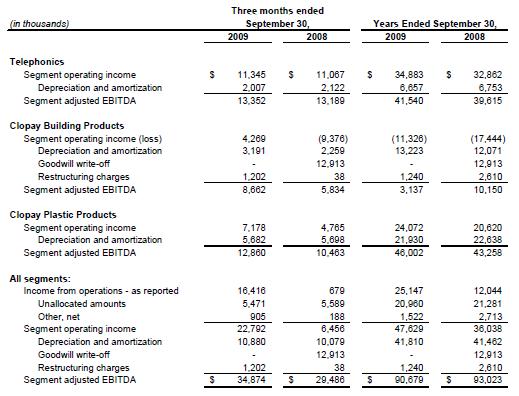

The Company’s segment adjusted EBITDA for the 2009 quarter was $34.9 million compared to $29.5 million in 2008. Segment adjusted EBITDA is defined as operating income, excluding corporate overhead, interest, taxes, depreciation and amortization, restructuring charges, goodwill impairment charges and the benefit of debt extinguishment.

Full Year 2009

Revenue for 2009 was $1.2 billion, compared to $1.3 billion in 2008. Income from continuing operations for 2009 was $22.0 million, or $0.37 per diluted share, compared to $0.1 million, or zero per diluted share, last year. The 2008 results included the $12.9 million goodwill impairment charge for the Building Products segment; excluding this charge, 2008 income from continuing operations would have been $13.0 million, or $0.40 per diluted share. Income from discontinued operations for 2009 was $0.8 million, or $0.01 per diluted share, compared to a loss of $40.6 million, or $1.24 per diluted share, last year. Net income for 2009 was $22.8 million, or $0.39 per diluted share, compared to a loss of $40.5 million, or $1.24 per diluted share in 2008. Diluted shares used for per share calculations were 59.0 million in 2009 compared to 32.8 million in 2008, an increase of 80% resulting primarily from the 2008 rights offering.

The Company’s 2009 segment adjusted EBITDA was $90.7 million compared to $93.0 million in the prior year.

During 2009, the Company purchased $50.6 million face value of the convertible notes from certain noteholders for $42.7 million. Net of related unamortized debt issuance costs of $0.5 million, the Company recorded a pre-tax gain of $7.4 million from debt extinguishment.

In June 2009, the Company announced plans to consolidate facilities of its Building Products segment. The consolidation, scheduled to be completed in early 2011, is expected to produce annual cost savings approximating $10 million. The Company estimates that it will incur pre-tax exit and restructuring costs approximating $12 million, substantially all of which will be cash charges. In addition, the Company expects to invest approximately $11 million in capital expenditures in order to effectuate the restructuring plan. These charges and expenditures will occur primarily in fiscal 2010 and 2011. For the fourth quarter and full year 2009, the Company incurred $1.2 million in restructuring costs and invested $2.0 million in related capital expenditures.

RESULTS OF OPERATIONS

Telephonics

For the quarter ended September 30, 2009, Telephonics revenue totaled $116.4 million, a 12% increase over 2008. This increase was mainly driven by strong growth in the Communications Division.

Segment operating profit increased $0.3 million, or 3%, compared to last year’s quarter, mainly due to favorable product mix, partially offset by increased operating expenses related to research and development and additional administrative expenses necessary to support sales growth.

In 2009, Telephonics’ revenue increased $21.6 million, or 6%, compared to the prior year, mainly due to higher sales in the Radar Systems division.

Segment operating profit increased $2 million to $34.9 million in 2008; segment operating profit margin remained at 9.0%, due to the strong sales performance and favorable program mix being offset by higher SG&A expenses. The increase in SG&A expenses resulted from higher research and development expenditures and additional administrative expenses to support revenue growth.

Clopay Building Products

For the quarter ended September 30, 2009, Building Products revenue totaled $106.8 million, a 14% decrease compared to 2008. Building Products continued to be adversely impacted by persistent weakness in the residential housing market. The sales decline was principally due to reduced unit volume, partially offset by favorable product mix.

Segment operating profit improved to $4.3 million compared to a loss of $9.4 million in the 2008 quarter. The 2008 result included the goodwill impairment charge of $12.9 million; excluding this charge, the 2008 operating results would have been a $3.5 million profit. Excluding the goodwill impairment charge from the 2008 comparative, the improvement in segment operating profit in the 2009 quarter was mainly enabled by the Company’s cost-cutting and facility rationalization initiatives

For the full year 2009, Building Products revenue totaled $393.4 million, a decrease of $41.9 million, or 10%, compared to 2008; this decline was due to the continued weak housing market. The revenue decline was principally due to reduced unit volume, partially offset by a favorable shift in mix to higher priced products

Segment operating loss for 2009 was $11.3 million, an improvement of $6.1 million compared to the prior year. The 2008 result included the goodwill impairment charge of $12.9 million; excluding this charge, the 2008 operating results would have been a $4.5 million loss. Excluding the goodwill impairment charge from the 2008 comparative, the increased loss in 2009 was mainly due to the sharp decline in volume, and the resultant unfavorable impact on absorption of fixed operating expenses. Notwithstanding the total loss for 2009, segment operating profit improved sequentially during 2009, reaching $0.6 million and $4.3 million in the third and fourth quarters, respectively, a significant improvement over the operating losses incurred in the first two quarters of 2009.

Clopay Plastic Products

For the quarter ended September 30, 2009, Plastics revenue totaled $105.0 million, a 16% decrease from the prior year. The lower revenue was principally due to lower volume in our European business, unfavorable foreign exchange translation and the pass through of lower resin costs in customer selling prices.

Segment operating profit of $7.2 million increased $2.4 million, or 51% compared to the prior year quarter, mainly as a result of favorable product mix, and lower SG&A costs due to lower volume and cost saving initiatives.

For the full year 2009, Plastics’ revenue totaled $412.8 million, a decrease of $54.9 million or 12%, compared to 2008. This revenue decline was principally due to lower volume in the European business, translation of the European results into the stronger U.S. dollar and the pass through of lower resin costs in customer selling prices.

Segment operating profit was $24.1 million, an increase of $3.5 million or 17%, compared to the prior year. The improvement in segment operating profit in 2009 was mainly enabled by the Company’s cost-cutting initiatives and favorable product mix, partially offset by lower unit volume. Segment operating profit margin increased 140 basis points compared to 2008.

Discontinued Operations

As a result of the downturn in the residential housing market, in 2008 the Company exited substantially all of the operating activities of its former Installation Services segment. Operating results of substantially the entire Installation Services segment have been reported as discontinued operations in the condensed consolidated financial statements for all periods presented, and the Installation Services segment is excluded from segment reporting. The Company substantially concluded its disposal of the Installation Services segment in the second quarter of 2009.

Balance Sheet and Capital Expenditures

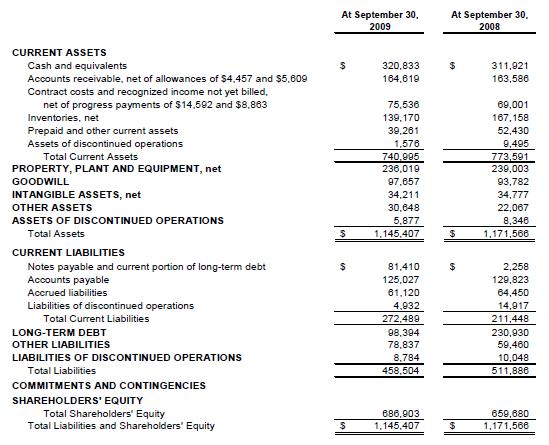

The Company’s total cash and equivalents at September 30, 2009 was $320.8 million. Total debt outstanding at September 30, 2009 was $179.8 million, including $79.4 million of convertible notes, for a net cash position of $141.0 million. Capital expenditures for 2009 were $32.7 million.

Conference Call Information

The Company will hold a conference call today, November 19, 2009, at 4:30 PM ET.

The call can be accessed by dialing 1-877-407-0784 (U.S. participants) or (201) 689-8560 (International participants). Callers should ask to be connected to Griffon Corporation’s fourth quarter 2009 teleconference and provide the conference ID number 337778.

A replay of the call will be available starting on November 19, 2009 at 7:30 PM ET by dialing 1- 877-660-6853 (U.S.) or (201) 612-7415 (International). The replay account number is 3055 with access code 337778. The replay will be available through December 3, 2009.

Forward-looking Statements

“Safe Harbor” Statements under the Private Securities Litigation Reform Act of 1995: All statements relate to, among other things, income, earnings, cash flows, revenue, changes in operations, operating improvements, industries in which Griffon Corporation (the “Company” or “Griffon”) operates and the United States and global economies. Statements that are not historical are hereby identified as “forward-looking statements” and may be indicated by words or phrases such as “anticipates,” “supports,” “plans,” “projects,” “expects,” “believes,” “should,” “would,” “could,” “hope,” “forecast,” “management is of the opinion,” “may,” “will,” “estimates,” “intends,” “explores,” “opportunities,” the negative of these expressions, use of the future tense and similar words or phrases. Such forward-looking statements are subject to inherent risks and uncertainties that could cause actual results to differ materially from those expressed in any forward-looking statements. These risks and uncertainties include, among others: current economic conditions and uncertainties in the housing, credit and capital markets; the Company’s ability to achieve expected savings from cost control, integration and disposal initiatives; the ability to identify and successfully consummate and integrate value-adding acquisition opportunities; increasing competition and pricing pressures in the markets served by Griffon’s operating companies; the ability of Griffon’s operating companies to expand into new geographic and product markets and to anticipate and meet customer demands for new products and product enhancements and innovations; the government reduces military spending on projects supplied by Griffon’s Telephonics Corporation; increases in cost of raw materials such as resin and steel; changes in customer demand; political events that could impact the worldwide economy; a downgrade in the Company’s credit ratings; international economic conditions including interest rate and currency exchange fluctuations; the relative mix of products and services which impacts margins and operating efficiencies; short-term capacity constraints or prolonged excess capacity; unforeseen developments in contingencies such as litigation; unfavorable results of government agency contract audits of Griffon’s subsidiary, Telephonics Corporation; protection and validity of patent and other intellectual property rights; the cyclical nature of the business of certain Griffon operating companies; and possible terrorist threats and actions, and their impact on the global economy. Such statements reflect the views of the Company with respect to future events and are subject to these and other risks, uncertainties and assumptions relating to the operations, results of operations, growth strategy and liquidity of the Company as previously disclosed in the Company’s Securities and Exchange Commission filings. Readers are cautioned not to place undue reliance on these forward-looking statements. These forward-looking statements speak only as of the date made. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

About Griffon Corporation

Griffon Corporation (the “Company” or “Griffon”), is a diversified management and holding company that conducts business through wholly-owned subsidiaries. The Company oversees the operations of its subsidiaries, allocates resources among them and manages their capital structures. The Company provides direction and assistance to its subsidiaries in connection with acquisition and growth opportunities as well as in connection with divestitures. Griffon also seeks out, evaluates and, when appropriate, will acquire additional businesses that offer potentially attractive returns on capital to further diversify itself.

Headquartered in New York, N.Y., the Company was incorporated in New York in 1959, and was reincorporated in Delaware in 1970. It changed its name to Griffon Corporation in 1995.

Griffon currently conducts its operations through Telephonics Corporation, Clopay Building Products Company and Clopay Plastic Products Company.

- Telephonics Corporation high-technology engineering and manufacturing capabilities

provide integrated information, communication and sensor system solutions to

military and commercial markets worldwide.

- Clopay Building Products Company is a leading manufacturer and marketer of

residential, commercial and industrial garage doors to professional installing dealers

and major home center retail chains.

- Clopay Plastic Products Company is an international leader in the development and production of embossed, laminated and printed specialty plastic films used in a variety of hygienic, health-care and industrial applications.

For more information on the Company and its operating subsidiaries, please see the Company's website at www.griffoncorp.com.

| Company Contact: | Investor Relations Contact: |

| Douglas J. Wetmore | James Palczynski |

| Chief Financial Officer | Principal and Director |

| Griffon Corporation | ICR Inc. |

| (212) 957-5000 | (203) 682-8229 |

| 712 Fifth Avenue, 18th Floor | |

| New York, NY 10019 |

GRIFFON CORPORATION AND SUBSIDIARIES

OPERATING HIGHLIGHTS

(Unaudited)

Unallocated amounts typically include general corporate expenses not attributable to any reportable segment.

GRIFFON CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

Note: Due to rounding, the sum of earnings per share of Continuing operations and Discontinued operations may not equal earnings per share of Net income.

GRIFFON CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Unaudited)

(in thousands)

GRIFFON CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(in thousands)

The following is a reconciliation of operating income, which is a GAAP measure of our operating results, to segment operating income and segment adjusted EBITDA. Management believes that the presentation of segment operating income and segment adjusted EBITDA is appropriate to provide additional information about the Company’s reportable segments. Segment operating income and segment adjusted EBITDA are not presentations made in accordance with GAAP, are not measures of financial performance or condition, liquidity or profitability of the Company, and should not be considered as an alternative to (1) net income, operating income or any other performance measures determined in accordance with GAAP or (2) operating cash flows determined in accordance with GAAP. Additionally, segment operating income and segment adjusted EBITDA are not intended to be measures of free cash flow for management’s discretionary use, as they do not consider certain cash requirements such as interest payments, tax payments, capital expenditures and debt service requirements.

GRIFFON CORPORATION AND SUBSIDIARIES

RECONCILIATION OF NON-GAAP MEASURES

SEGMENT ADJUSTED EBITDA - BY REPORTABLE SEGMENT

(Unaudited)

Unallocated amounts typically include general corporate expenses not attributable to any reportable segment.